Big companies like Apple manufacture their own products, but that’s a pricey proposition for a new business. A more affordable option is to buygoo ...

You might consider targeting a niche, such as homes sold as part of estates.

We earn commissions if you shop through the links below. Read more

Written by: Carolyn Young

Carolyn Young is a business writer who focuses on entrepreneurial concepts and the business formation. She has over 25 years of experience in business roles, and has authored several entrepreneurship textbooks.

Edited by: David Lepeska

David has been writing and learning about business, finance and globalization for a quarter-century, starting with a small New York consulting firm in the 1990s.

Published on April 14, 2023

Updated on July 3, 2024

Investment range

$500 - $1,800

Revenue potential

$60,000 - $180,000 p.a.

Time to build

1 – 3 months

Profit potential

$54,000 - $162,000 p.a.

Industry trend

Declining

Commitment

Flexible

Want to get in on the real estate game with little money? Look no further than real estate wholesaling! In real estate wholesaling, the wholesaler commits to buying a home at a certain price, then finds a buyer willing to purchase the home for more than that.

The difference between the two prices is the wholesaler’s revenue. The homes involved in these sales are usually distressed and these transactions typically have no out-of-pocket costs, so getting started requires very little funding.

But before you hit the pavement in search of bargains, you’ll need some business savvy. Luckily, this step-by-step guide has all the business insights you need to become a wholesale real estate mogul.

Looking to register your business? A limited liability company (LLC) is the best legal structure for new businesses because it is fast and simple.

Form your business immediately using ZenBusiness LLC formation service or hire one of the Best LLC Services.

Real estate wholesaling falls under the real estate sales and brokerage industry.

Trends

Challenges

Costs to start a real estate wholesaling business are minimal, ranging from $500 to $1,800. The main expense is marketing.

| Start-up Costs | Ballpark Range | Average |

|---|---|---|

| Setting up a business name and corporation | $100 - $500 | $300 |

| Business licenses and permits | $100 - $300 | $200 |

| Insurance | $100-$500 | $300 |

| Initial Marketing Budget | $200 - $500 | $350 |

| Total | $500 - $1,800 | $1,150 |

The average wholesaling deal brings in $12,000. After marketing costs, your profit margin will be about 90%.

In your first year or two, you might do five deals a year, bringing in $60,000 in revenue. This would mean $54,000 in profit, assuming that 90% margin. As you gain traction, you might do 15 deals a year. With annual revenue of $180,000, you’d make a tidy profit of $162,000.

There are a few barriers to entry for a real estate wholesaling business. Your biggest challenges will be:

Now that you know what’s involved in starting a real estate wholesaling business, it’s a good idea to hone your concept in preparation to enter a competitive market.

Market research could give you the upper hand even if you’ve got the perfect product. Conducting robust market research is crucial, as it will help you better understand your customers, your competitors, and the broader business landscape.

Research real estate wholesalers in your area to examine their deals and price points.

This should identify areas where you can strengthen your business and gain a competitive edge to make better business decisions.

You’re looking for a market gap to fill. For instance, maybe the local market is missing a wholesaler who specializes in high-end properties.

You might consider targeting a niche, such as homes sold as part of estates.

This could jumpstart your word-of-mouth marketing and attract clients right away.

When you’re wholesaling real estate, you’re essentially selling a contract to the home seller. The contract gives you the right to purchase the property at a certain price and find a buyer that will pay a higher price within a specified amount of time.

When you enter into the contract, you’ll give the seller what’s called a good faith or earnest money deposit, which is usually 1-3 percent of the purchase price. If you don’t find a buyer in the specified amount of time, you’ll lose that deposit.

You’re going to have two target markets. First, you’ll have to market yourself and your skills to sellers of distressed properties. This is a broad group, so you should spread out your marketing to include Instagram and Facebook.

Then you’ll have to market homes to buyers, who will usually be investors. Your best bet to find real estate investors is LinkedIn.

In the early stages, you may want to run your business from home to keep costs low. But as your business grows, you’ll likely need to hire workers for various roles and may need to rent out an office. You can find commercial space to rent in your area on sites such as Craigslist, Crexi, and Instant Offices.

When choosing a commercial space, you may want to follow these rules of thumb:

Here are some ideas for brainstorming your business name:

Once you’ve got a list of potential names, visit the website of the US Patent and Trademark Office to make sure they are available for registration and check the availability of related domain names using our Domain Name Search tool. Using “.com” or “.org” sharply increases credibility, so it’s best to focus on these.

Finally, make your choice among the names that pass this screening and go ahead and reserve your business name with your state, start the trademark registration process, and complete your domain registration and social media account creation.

Your business name is one of the key differentiators that sets your business apart. Once you pick a name, reserve it and start with the branding, it’s hard to switch to a new name. So be sure to carefully consider your choice before moving forward.

Here are the key components of a business plan:

If you’ve never created a business plan, it can be an intimidating task. You might consider hiring a business plan specialist to create a top-notch business plan for you.

Registering your business is an absolutely crucial step — it’s the prerequisite to paying taxes, raising capital, opening a bank account, and other guideposts on the road to getting a business up and running.

Plus, registration is exciting because it makes the entire process official. Once it’s complete, you’ll have your own business!

Your business location is important because it can affect taxes, legal requirements, and revenue. Most people will register their business in the state where they live, but if you are planning to expand, you might consider looking elsewhere, as some states could offer real advantages when it comes to real estate wholesaling.

If you’re willing to move, you could really maximize your business! Keep in mind, it’s relatively easy to transfer your business to another state.

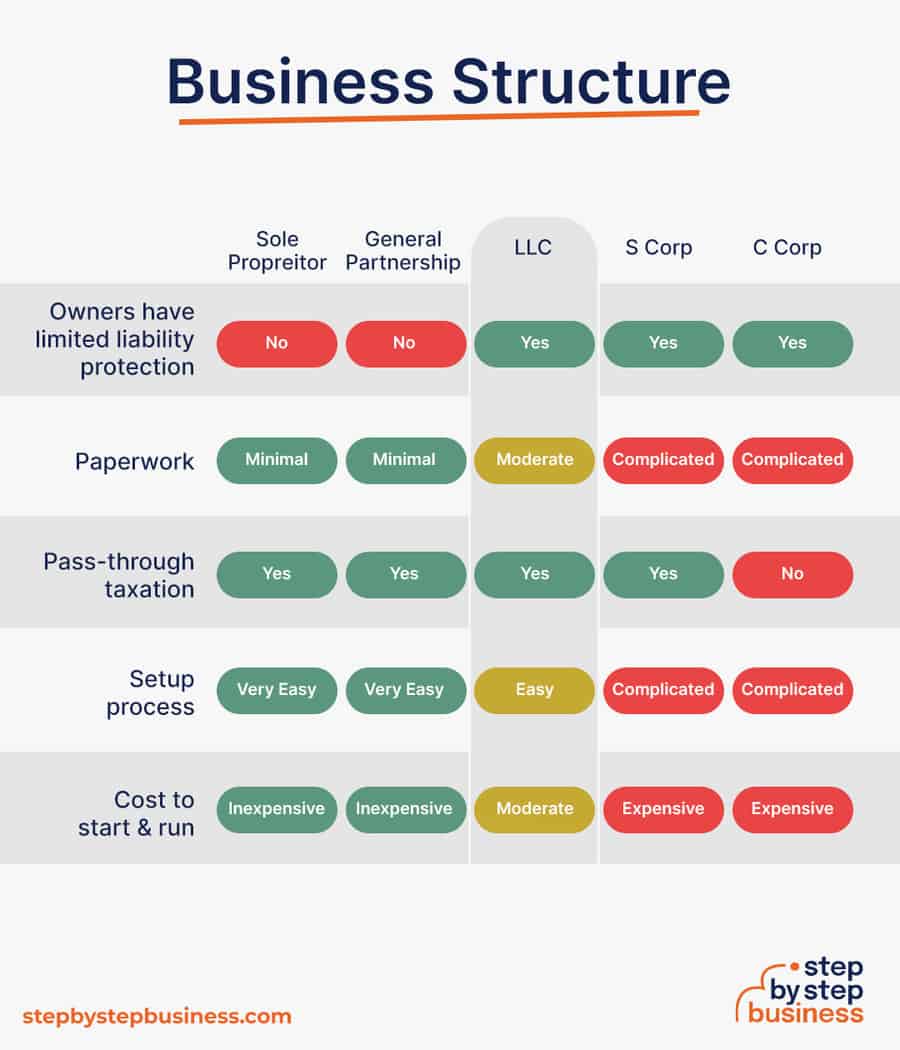

Business entities come in several varieties, each with its pros and cons. The legal structure you choose for your real estate wholesaling business will shape your taxes, personal liability, and business registration requirements, so choose wisely.

Here are the main options:

We recommend that new business owners choose LLC as it offers liability protection and pass-through taxation while being simpler to form than a corporation.

You can form an LLC in as little as five minutes using an online LLC formation service. They will check that your business name is available before filing, submit your articles of organization, and answer any questions you might have.

Choose Your State

The final step before you’re able to pay taxes is getting an Employer Identification Number, or EIN. You can file for your EIN online or by mail or fax: visit the IRS website to learn more. Keep in mind, if you’ve chosen to be a sole proprietorship you can simply use your social security number as your EIN.

Once you have your EIN, you’ll need to choose your tax year. Financially speaking, your business will operate in a calendar year (January–December) or a fiscal year, a 12-month period that can start in any month. This will determine your tax cycle, while your business structure will determine which taxes you’ll pay.

The IRS website also offers a tax-payers checklist, and taxes can be filed online.

It is important to consult an accountant or other professional to help you with your taxes to ensure you are completing them correctly.

Securing financing is your next step and there are plenty of ways to raise capital:

Bank and SBA loans are probably the best option, other than friends and family, for funding a real estate wholesaling business.

Starting a real estate wholesaling business requires obtaining a number of licenses and permits from local, state, and federal governments.

Federal regulations, licenses, and permits associated with starting your business include doing business as (DBA), health licenses and permits from the Occupational Safety and Health Administration (OSHA), trademarks, copyrights, patents, and other intellectual properties, as well as industry-specific licenses and permits.

You generally do not need a real estate license to wholesale real estate, but you need to make sure that you do not act as a real estate agent in any way. Sometimes it’s a fine line between wholesaling real estate and being a real estate broker, so be careful. Check your state’s laws regarding real estate wholesaling to make sure you stay in compliance.

You may also need state-level and local county or city-based licenses and permits. The license requirements and how to obtain them vary, so check the websites of your state, city, and county governments or contact the appropriate person to learn more.

You could also check this SBA guide for your state’s requirements, but we recommend using MyCorporation’s Business License Compliance Package. They will research the exact forms you need for your business and state and provide them to ensure you’re fully compliant.

This is not a step to be taken lightly, as failing to comply with legal requirements can result in hefty penalties.

If you feel overwhelmed by this step or don’t know how to begin, it might be a good idea to hire a professional to help you check all the legal boxes.

Before you start making money, you’ll need a place to keep it, and that requires opening a bank account.

Keeping your business finances separate from your personal account makes it easy to file taxes and track your company’s income, so it’s worth doing even if you’re running your real estate wholesaling business as a sole proprietorship. Opening a business bank account is quite simple, and similar to opening a personal one. Most major banks offer accounts tailored for businesses — just inquire at your preferred bank to learn about their rates and features.

Banks vary in terms of offerings, so it’s a good idea to examine your options and select the best plan for you. Once you choose your bank, bring in your EIN (or Social Security Number if you decide on a sole proprietorship), articles of incorporation, and other legal documents and open your new account.

Business insurance is an area that often gets overlooked yet it can be vital to your success as an entrepreneur. Insurance protects you from unexpected events that can have a devastating impact on your business.

Here are some types of insurance to consider:

As opening day nears, prepare for launch by reviewing and improving some key elements of your business.

Being an entrepreneur often means wearing many hats, from marketing to sales to accounting, which can be overwhelming. Fortunately, many websites and digital tools are available to help simplify many business tasks.

You may want to use industry-specific software, such as Deal Machine or REI, to manage your leads, emails, deal flows, and pricing.

Website development is crucial because your site is your online presence and needs to convince prospective clients of your expertise and professionalism. You can create your own website using services like WordPress, Wix, or Squarespace. This route is very affordable, but figuring out how to build a website can be time-consuming. If you lack tech-savvy, you can hire a web designer or developer to create a custom website for your business.

Your customers are unlikely to find your website, however, unless you follow Search Engine Optimization (SEO) practices. SEO will help your website appear closer to the top in relevant search results, a crucial element for increasing sales.

Make sure that you optimize calls to action on your website. Experiment with text, color, size, and position of calls to action such as “Schedule Consultation Now”. This can sharply increase purchases.

Here are some powerful marketing strategies for your future business:

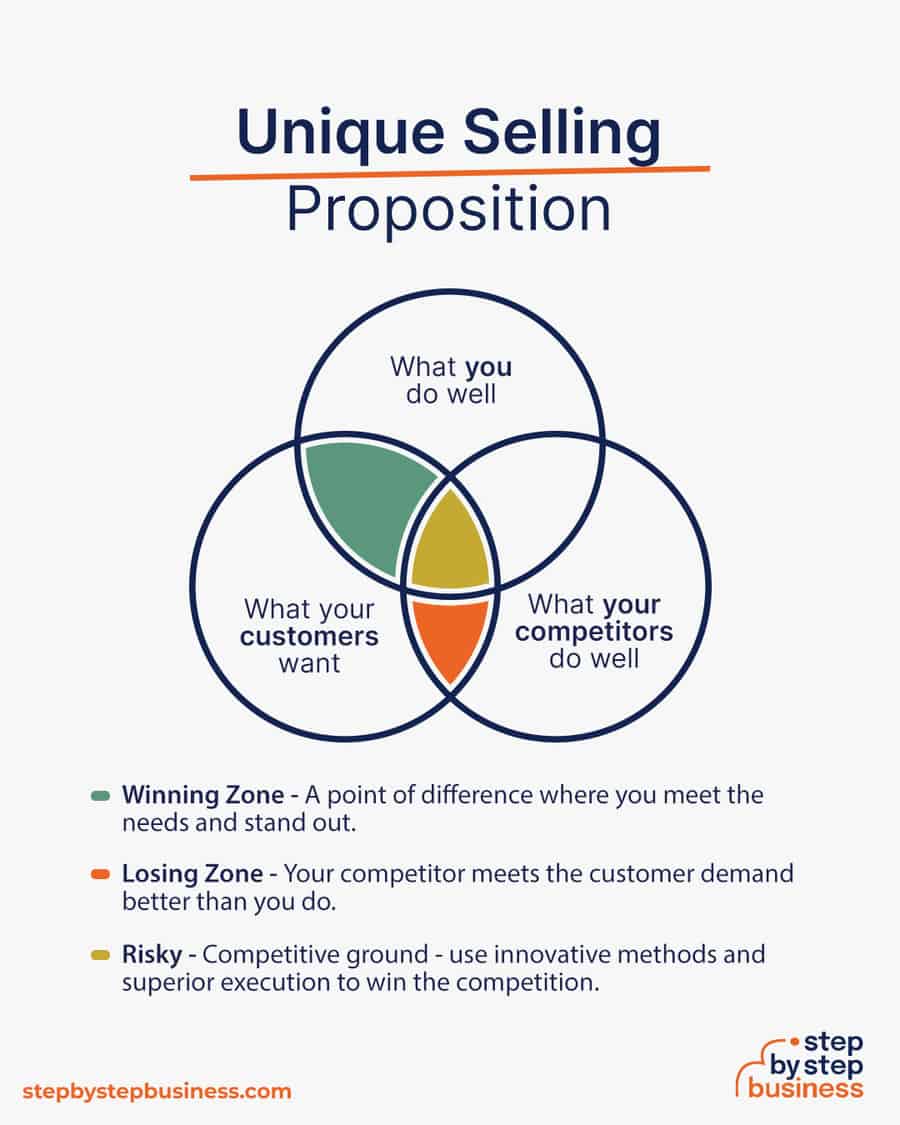

Unique selling propositions, or USPs, are the characteristics of a product or service that sets it apart from the competition. Customers today are inundated with buying options, so you’ll have a real advantage if they are able to quickly grasp how your real estate wholesaling meets their needs or wishes. It’s wise to do all you can to ensure your USPs stand out on your website and in your marketing and promotional materials, stimulating buyer desire.

Global pizza chain Domino’s is renowned for its USP: “Hot pizza in 30 minutes or less, guaranteed.” Signature USPs for your real estate wholesaling business could be:

You may not like to network or use personal connections for business gain. But your personal and professional networks likely offer considerable untapped business potential. Maybe that Facebook friend you met in college is now running a real estate wholesaling business, or a LinkedIn contact of yours is connected to dozens of potential clients. Maybe your cousin or neighbor has been working in real estate wholesaling for years and can offer invaluable insight and industry connections.

The possibilities are endless, so it’s a good idea to review your personal and professional networks and reach out to those with possible links to or interest in real estate. You’ll probably generate new customers or find companies with which you could establish a partnership.

If you’re starting out small from a home office, you may not need any employees. But as your business grows, you will likely need workers to fill various roles. Potential positions for a real estate wholesaling business include:

At some point, you may need to hire all of these positions or simply a few, depending on the size and needs of your business. You might also hire multiple workers for a single role or a single worker for multiple roles, again depending on need.

Free-of-charge methods to recruit employees include posting ads on popular platforms such as LinkedIn, Facebook, or Jobs.com. You might also consider a premium recruitment option, such as advertising on Indeed, Glassdoor, or ZipRecruiter. Further, if you have the resources, you could consider hiring a recruitment agency to help you find talent.

Real estate wholesaling is challenging, but it can be very profitable, and you can start for virtually no money. You’ll be helping homeowners who are in trouble and offering great deals to buyers.

The real estate market is ripe with opportunity, so you could turn your wholesaling business into a major real estate investment firm. Now that you understand the business side of it, the sky’s the limit!

No, an LLC is not a requirement for wholesaling real estate. However, LLC has many benefits, particularly personal liability protection. In real estate transactions, things can go wrong, and you have the potential to be sued.

If you run your business as a sole proprietorship, you have no personal liability protection, so your personal assets, including your personal home, are at risk. Having an LLC removes this risk. To make sure that an LLC is the right business entity for you, it’s recommended that you consult your attorney and tax advisor.

Real estate wholesaling can be a profitable side hustle. It’s not very labor intensive, but requires a lot of selling ability.

To find properties to wholesale, you can network with real estate agents, attend local real estate auctions, market directly to distressed property owners, or use online real estate platforms to identify potential deals. Building a strong network and employing effective marketing strategies are key to finding suitable properties.

Building a buyer’s list involves networking with real estate investors, attending real estate investment groups or clubs, leveraging social media and online forums, and using email marketing campaigns. Offering valuable deals and maintaining good relationships with buyers can help grow your list.

Risks in real estate wholesaling include not being able to find a buyer within the contract timeframe, which can result in losing your earnest money deposit. Additionally, market fluctuations can affect property values, and legal issues can arise if contracts are not handled correctly.

Published on April 22, 2023

Big companies like Apple manufacture their own products, but that’s a pricey proposition for a new business. A more affordable option is to buygoo ...

Read Now

Published on November 4, 2022

Think about going wholesale? It’s a pretty reliable route to businesssuccess. A wholesale business purchases products directly frommanuf ...

Read Now

Published on July 12, 2022

Businesses that rely on regular rental payments are guaranteed a steady stream of income, which is why so many of them draw so much entrepreneuriali ...

Read Now

No thanks, I don't want to stay up to date on industry trends and news.

Comments