Carolyn Young is a business writer who focuses on entrepreneurial concepts and the business formation. She has over 25 years of experience in business roles, and has authored several entrepreneurship textbooks.

David has been writing and learning about business, finance and globalization for a quarter-century, starting with a small New York consulting firm in the 1990s.

Published on December 13, 2021

Fast Facts

Investment range

$28,650 - $114,100

Revenue potential

$36,000 - $72,000 p.a.

Time to build

1 – 3 Months

Profit potential

$32,000 - $65,000 p.a.

Industry trend

Growing

Commitment

Flexible

Important elements to think about when starting your rental property business:

Define your market — Decide on the types of rental properties you will focus on, such as residential (single-family homes, apartments), commercial (office spaces, retail spaces), or vacation rentals.

Licenses and permits — Depending on your location, you may need specific permits or licenses to operate rental properties, such as landlord permits.

Property selection — Choose properties in desirable locations with strong rental demand and potential for appreciation.

Legal business aspects — Register for taxes, open a business bank account, and get an EIN.

Advertising — Use online platforms (e.g., Zillow, Craigslist, social media) and offline methods (local advertising, signage) to market your rental properties.

Maintenance and repairs — Develop a system for regular maintenance and prompt repairs to keep properties in good condition and ensure tenant satisfaction.

Realtor partnerships — Consider partnering with real estate agents to help find and screen potential tenants.

Technology integration — Use property management software and other technologies to streamline operations, improve efficiency, and enhance tenant experience.

Learn from real entrepreneurs who run this business:

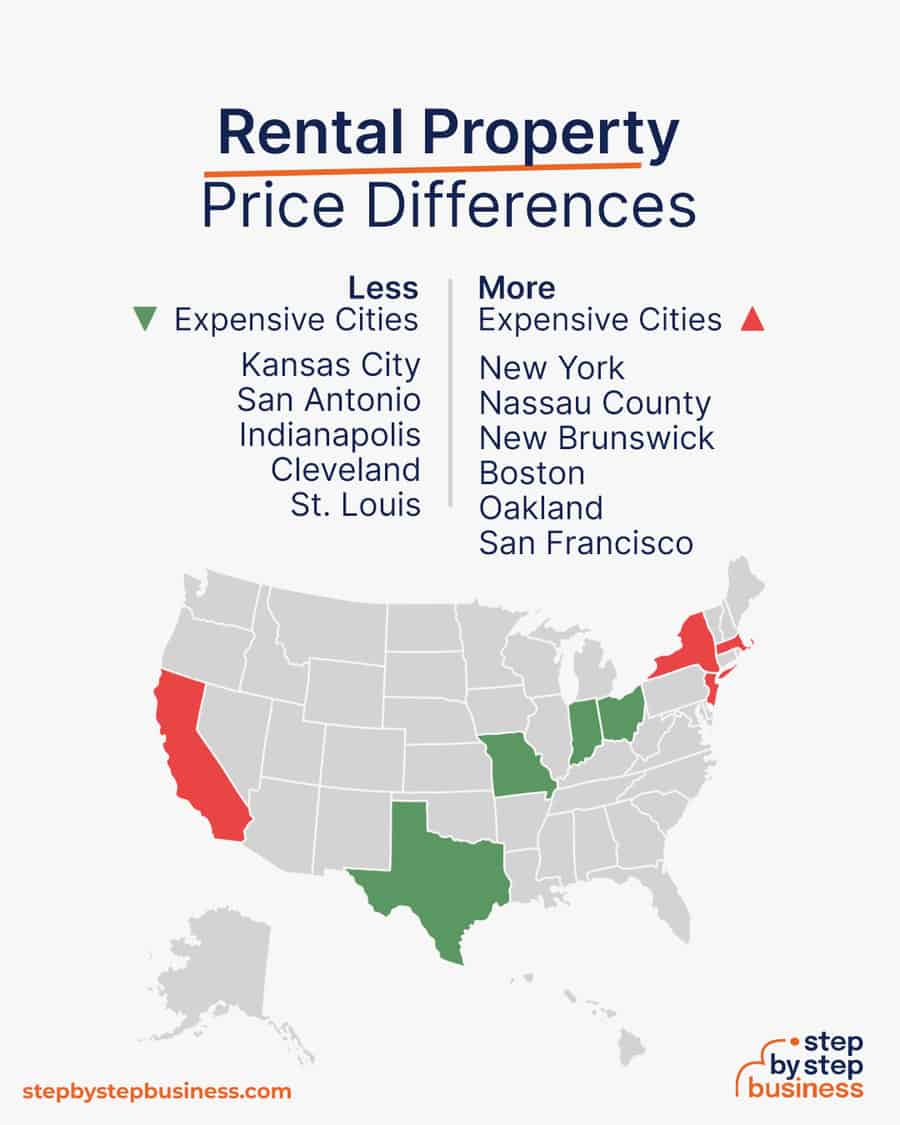

More expensive – Rents are highest in New York and Nassau County (NY), New Brunswick (NJ), Boston (MA), and Oakland and San Francisco (CA), with rents between $3,700 and $4,000 in May 2022.

Less expensive – Rents are lowest in Kansas City (MO), San Antonio (TX), Indianapolis (IN), Cleveland (OH), and St. Louis (MO), with rents between $1,400 and $1,600.

How much does it cost to start a rental property business?

Startup costs for a rental property business range from $25,000 to half a million or more. The main cost is obviously the property itself, so your initial investment will depend on the type of property you decide to buy. Lenders generally require a 20%-25% down payment.

Startup Costs

Ballpark Range

Average

Setting up a business name and corporation

$150 - $200

$175

Licenses and permits

$200 - $300

$250

Insurance

$100 - $300

$200

Business cards and brochures

$200 - $300

$250

Website setup

$1,000 - $3,000

$2,000

First property down payment

$25,000 - $100,000

$62,500

Renovation of first property

$2,000 - $10,000

$6,000

Total

$28,650 - $114,100

$71,375

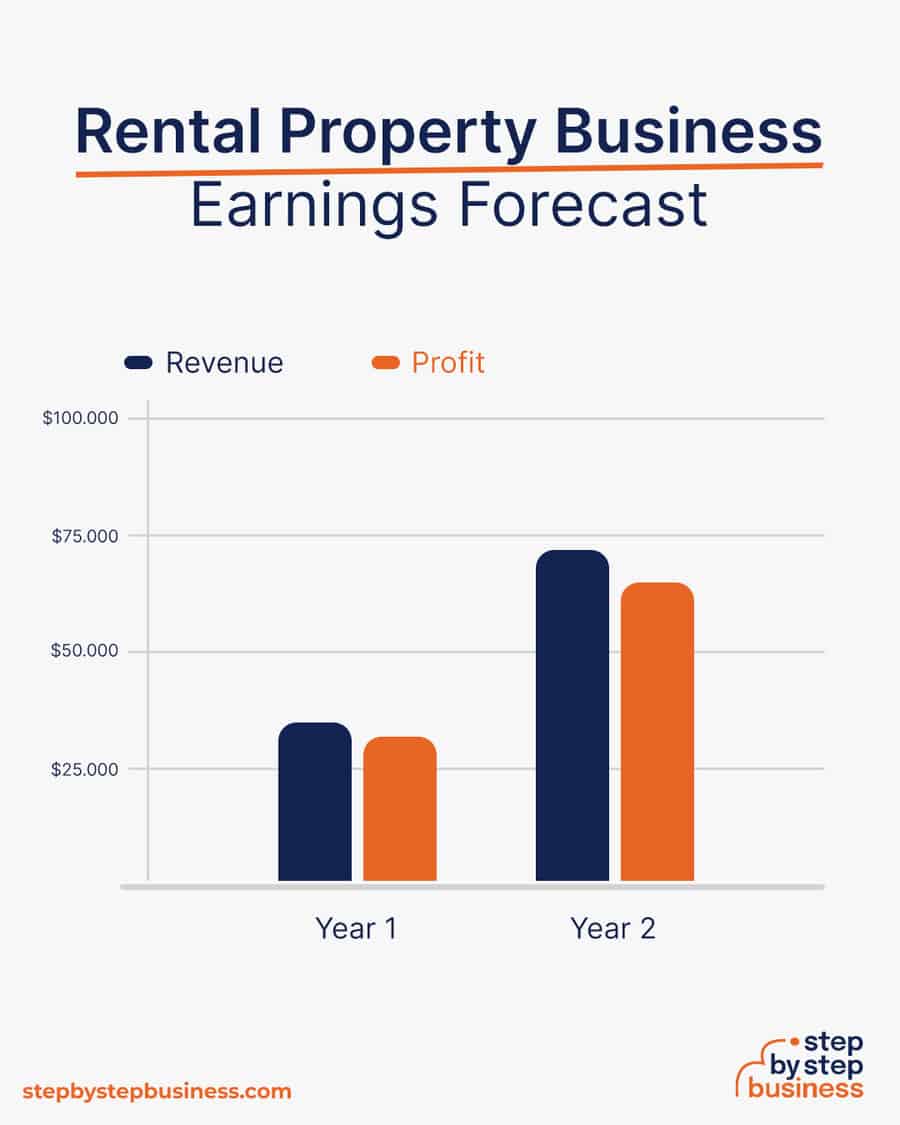

How much can you earn from a rental property business?

Your income will of course depend on the rents you charge, minus your mortgage payment. A general rule for real estate investors is to make at least $150 per month per unit. Keep in mind that you will see more financial benefits at tax time and in the long run, as your properties appreciate and rents increase.

Subtracting the chunk of rent that will cover your mortgage payments, after expenses, such as maintenance, you should expect a profit margin of around 90%.

If you start with a 20-unit building and net $150 per month per unit, you’ll bring in $36,000 in annual revenue and around $32,000 in profit, assuming that 90% margin. If in a few years you’re able to add 20 more units, you’d have annual revenue of close to $72,000 and nearly $65,000 in profit.

The biggest barrier to entry into the rental property market is the hefty investment cost. You’ll have to purchase and develop a property that you can rent out, whether an apartment building or single-family homes.

Other barriers to entry are the government regulations that you have to comply with, tax payments, and legal requirements.

2. Shape Your Idea

Now that you know what’s involved in starting a rental property business, it’s a good idea to hone your concept in preparation to enter a competitive market.

Market research will give you the upper hand, even if you’re already positive that you have a perfect product or service. Conducting market research is important, because it can help you understand your customers better, who your competitors are, and your business landscape.

Why? Identify an opportunity

Research rental properties in your area to examine their price points and customer reviews. You’re looking for a market gap to fill.

You can capitalize on the rising demand for single-family home rentals and build a portfolio with long-term value while generating significant rental income.((https://www.usnews.com/news/business/articles/2021-11-24/housing-market-trends-fuel-single-family-home-rental-growth)) In the third quarter of 2021, construction began on 16,000 build-to-rent homes, the highest number since 1990, according to the National Association of Home Builders. So, while larger residential buildings still do present an opportunity, the rising number of single-family home rentals points to another, potentially larger long-term income stream.

What? Plan your rental property investments

You can invest in an apartment building, single-family rental units, vacation homes, serviced apartments, and more. The highest share of US renters (35%) live in buildings with more than 10 units, but the share of renters in single-family homes (26%) is on the rise.

You might also consider offering environment-friendly features. Rental properties with pools, gyms, and other amenities are also in demand.

Home-stay rentals like Airbnb and VRBO are also booming, so you may want to keep that in mind as an option, assuming your area allows it. You can learn more in the Step By Step article on How to Start an Airbnb Business.

How much should you charge for your rental property?

Rising house prices are also pushing rents up and pricing many US households out of the housing market. In May 2022, the national median monthly rent surpassed $2,000 for the first time.

You’ll have to consider your maintenance costs, overhead expenses, and target profit margin in determining how much you’ll ask for rent. Once you know your costs, you can use this Step By Step profit margin calculator to determine your mark-up and final price points. Remember, the prices you use at launch should be subject to change if warranted by the market.

Who? Identify your target market

Your target market depends on which properties you invest in. If you invest in urban apartments, your demographic will tend to be younger, so you can find them on sites like Instagram, rather than Facebook.

Where? Choose your business premises

You might consider investing in a rental property in either an urban or suburban area. Rentals are split almost evenly between these, but the latest shift is toward the latter. This is due in part to the greater number of people working from home post-pandemic, who no longer need to live in pricier urban areas to be close to the office.

As to your office, you may want to run your business from home in the early stages to keep costs low. But as your business grows, you’ll likely need to hire workers for various roles and may need to rent out a commercial space. You can find commercial space to rent in your area on Craigslist, Crexi, and Commercial Cafe.

When choosing a commercial space, you may want to follow these rules of thumb:

Central location accessible via public transport

Ventilated and spacious, with good natural light

Flexible lease that can be extended as your business grows

Ready-to-use space with no major renovations or repairs needed

3. Name Your Rental Empire

Here are some ideas for brainstorming your business name:

Short, unique, and catchy names tend to stand out

Names that are easy to say and spell tend to do better

The name should be relevant to your product or service offerings

Ask around — family, friends, colleagues, social media — for suggestions

Including keywords, such as “properties” or “rentals”, boosts SEO

Choose a name that allows for expansion: “Gateway Property Holdings” over “Corporate Housing Solutions” or “Student Housing Rentals”

A location-based name can help establish a strong connection with your local community and help with the SEO but might hinder future expansion

Once you’ve got a list of potential names, visit the website of the US Patent and Trademark Office to make sure they are available for registration and check the availability of related domain names using our Domain Name Search tool below. Using “.com” or “.org” sharply increases credibility, so it’s best to focus on these.

Finally, make your choice among the names that pass this screening and go ahead with domain registration and social media account creation. Your business name is one of the key differentiators that sets your business apart. Once you pick your company name, and start with the branding, it is hard to change the business name. Therefore, it’s important to carefully consider your choice before you start a business entity.

Executive Summary: Summarize the vision and strategy for your rental property business, including the types of properties you’ll rent and your growth goals.

Business Overview: Describe the rental property services you will offer, such as residential or commercial leasing and property management.

Product and Services: List the types of properties you plan to rent out, including single-family homes, apartments, or commercial spaces.

Market Analysis: Analyze the local real estate market to assess demand and identify your target tenant market.

Competitive Analysis: Compare your business to other rental property providers, noting how your properties or services will better meet tenant needs.

Sales and Marketing: Outline how you will market your properties and attract tenants, such as through online listings, open houses, or agency partnerships.

Management Team: Highlight the expertise and roles of your management team in real estate and business operations.

Operations Plan: Detail the day-to-day operations, including tenant acquisition, maintenance, and rent collection.

Financial Plan: Provide financial projections, including initial investment requirements, rental income, and long-term profitability estimates.

Appendix: Include additional documents like property photographs, market research data, or maintenance service agreements that support your business plan.

If you’ve never created a business plan, it can be an intimidating task. You might consider hiring a business plan specialist to create a top-notch business plan for you.

5. Make It Legal

Registering your business is an absolutely crucial step — it’s the prerequisite to paying taxes, raising capital, opening a bank account, and other guideposts on the road to getting a business up and running.

Plus, registration is exciting because it makes the entire process official. Once it’s complete, you’ll have your own business!

Choose where to register your company

Your business location is important because it can affect taxes, legal requirements, and revenue. Most people will register their business in the state where they live, but if you are planning to expand, you might consider looking elsewhere, as some states could offer real advantages when it comes to rental properties.

If you’re willing to move, you could really maximize your business! Keep in mind, it’s relatively easy to transfer your business to another state.

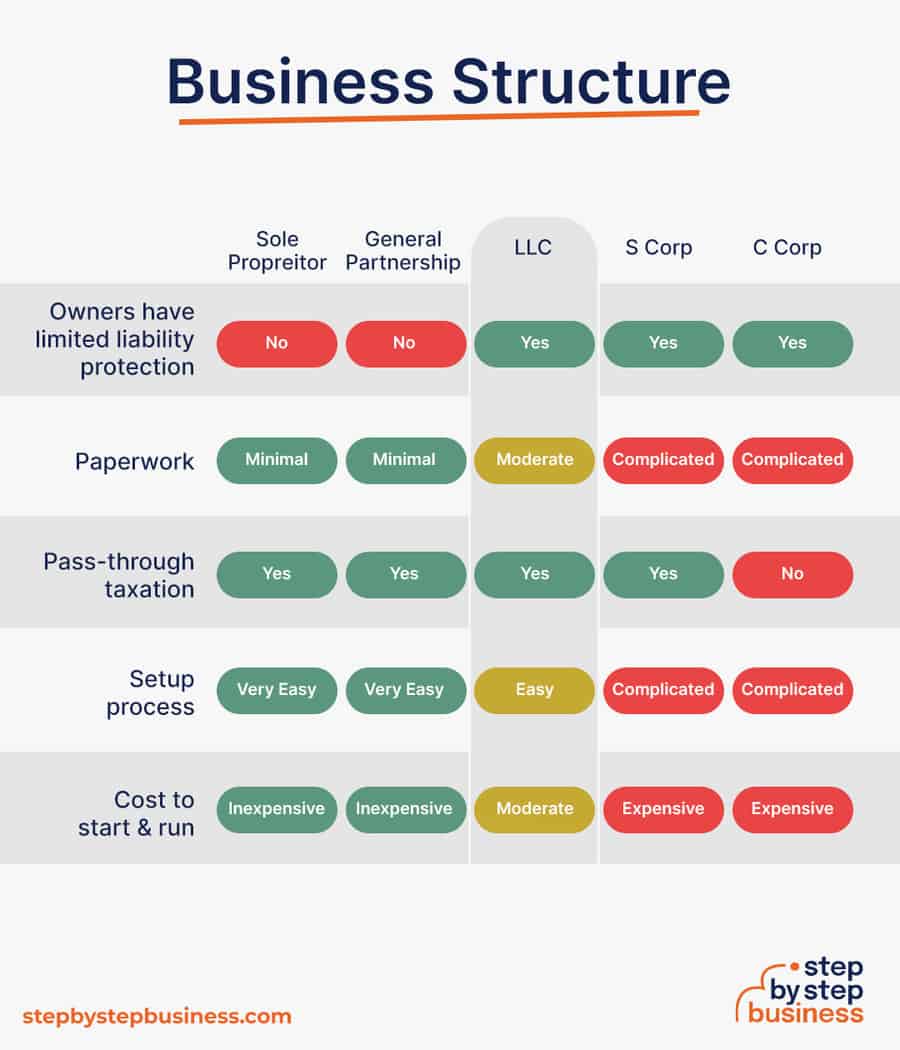

Choose your business structure

Business entities come in several varieties, each with its pros and cons. The legal structure you choose for your rental property business will shape your taxes, personal liability, and business registration requirements, so choose wisely.

Here are the main options:

Sole Proprietorship – The most common structure for small businesses makes no legal distinction between company and owner. All income goes to the owner, who’s also liable for any debts, losses, or liabilities incurred by the business. The owner pays taxes on business income on his or her personal tax return.

General Partnership – Similar to a sole proprietorship, but for two or more people. Again, owners keep the profits and are liable for losses. The partners pay taxes on their share of business income on their personal tax returns.

Limited Liability Company (LLC) – Combines the characteristics of corporations with those of sole proprietorships or partnerships. Again, the owners are not personally liable for debts.

C Corp – Under this structure, the business is a distinct legal entity and the owner or owners are not personally liable for its debts. Owners take profits through shareholder dividends, rather than directly. The corporation pays taxes, and owners pay taxes on their dividends, which is sometimes referred to as double taxation.

S Corp – An S-Corporation refers to the tax classification of the business but is not a business entity. An S-Corp can be either a corporation or an LLC, which just need to elect to be an S-Corp for tax status. In an S-Corp, income is passed through directly to shareholders, who pay taxes on their share of business income on their personal tax returns.

We recommend that new business owners choose LLC as it offers liability protection and pass-through taxation while being simpler to form than a corporation. You can form an LLC in as little as five minutes using an online LLC formation service. They will check that your business name is available before filing, submit your articles of organization, and answer any questions you might have.

The final step before you’re able to pay taxes is getting an Employer Identification Number, or EIN. You can file for your EIN online or by mail or fax: visit the IRS website to learn more. Keep in mind, if you’ve chosen to be a sole proprietorship, you can simply use your social security number as your EIN.

Once you have your EIN, you’ll need to choose your tax year. Financially speaking, your business will operate in a calendar year (January–December) or a fiscal year, a 12-month period that can start in any month. This will determine your tax cycle, while your business structure will determine which taxes you’ll pay.

The IRS website also offers a tax-payers checklist, and taxes can be filed online.

It is important to consult an accountant or other professional to help you with your taxes to ensure you are completing them correctly.

7. Find the Money

Securing financing is your next step and there are plenty of ways to raise capital:

Bank loans: This is the most common method, but getting approved requires a rock-solid business plan and strong credit history.

SBA-guaranteed loans: The Small Business Administration can act as guarantor, helping gain that elusive bank approval via an SBA-guaranteed loan.

Government grants: A handful of financial assistance programs help fund entrepreneurs. Visit Grants.gov to learn which might work for you.

Friends and Family: Reach out to friends and family to provide a business loan or investment in your concept. It’s a good idea to have legal advice when doing so because SEC regulations apply.

Personal: Self-fund your business via your savings or the sale of property or other assets.

Bank and SBA loans are probably the best option, other than friends and family, for funding a rental property business.

Starting a rental property business requires obtaining a number of licenses and permits from local, state, and federal governments.

Federal regulations, licenses, and permits associated with starting your business include doing business as (DBA), health licenses and permits from the Occupational Safety and Health Administration (OSHA), trademarks, copyrights, patents, and other intellectual properties, as well as industry-specific licenses and permits.

You may also need state-level and local county or city-based licenses and permits. The license requirements and how to obtain them vary, so check the websites of your state, city, and county governments or contact the appropriate person to learn more.

You could also check this SBA guide for your state’s requirements, but we recommend using MyCorporation’s Business License Compliance Package. They will research the exact forms you need for your business and state and provide them to ensure you’re fully compliant.

This is not a step to be taken lightly, as failing to comply with legal requirements can result in hefty penalties.

If you feel overwhelmed by this step or don’t know how to begin, it might be a good idea to hire a professional to help you check all the legal boxes.

Before you start making money you’ll need a place to keep it, and that requires opening a bank account.

Keeping your business finances separate from your personal account makes it easy to file taxes and track your company’s income, so it’s worth doing even if you’re running your rental property business as a sole proprietorship. Opening a business bank account is quite simple, and similar to opening a personal one. Most major banks offer accounts tailored for businesses — just inquire at your preferred bank to learn about their rates and features.

Banks vary in terms of offerings, so it’s a good idea to examine your options and select the best plan for you. Once you choose your bank, bring in your EIN (or Social Security Number if you decide on a sole proprietorship), articles of incorporation, and other legal documents and open your new account.

10. Protect Your Assets with Insurance

Business insurance is an area that often gets overlooked yet it can be vital to your success as an entrepreneur. Insurance protects you from unexpected events that can have a devastating impact on your business.

Here are some types of insurance to consider:

General liability: The most comprehensive type of insurance, acting as a catch-all for many business elements that require coverage. If you get just one kind of insurance, this is it. It even protects against bodily injury and property damage.

Business Property: Provides coverage for your equipment and supplies.

Equipment Breakdown Insurance: Covers the cost of replacing or repairing equipment that has broken due to mechanical issues.

Worker’s compensation: Provides compensation to employees injured on the job.

Property: Covers your physical space, whether it is a cart, storefront, or office.

Commercial auto: Protection for your company-owned vehicle.

Professional liability: Protects against claims from a client who says they suffered a loss due to an error or omission in your work.

Business owner’s policy (BOP): This is an insurance plan that acts as an all-in-one insurance policy, a combination of any of the above insurance types.

As opening day nears, prepare for launch by reviewing and improving some key elements of your business.

Essential software and tools

Being an entrepreneur often means wearing many hats, from marketing to sales to accounting, which can be overwhelming. Fortunately, many websites and digital tools are available to help simplify many business tasks.

You can use industry-specific software, such as TenantCloud, Buildium, and Propertyware, to manage your properties and tenants, oversee maintenance, set a schedule for rent payments, and more.

Popular web-based accounting programs for smaller businesses include Quickbooks, Freshbooks, and Xero.

If you’re unfamiliar with basic accounting, you may want to hire a professional, especially as you begin. The consequences for filing incorrect tax documents can be harsh, so accuracy is crucial.

Website development is crucial because your site is your online presence and needs to convince prospective clients of your expertise and professionalism.

You can create your own website using services like WordPress, Wix, or Squarespace. This route is very affordable, but figuring out how to build a website can be time-consuming. If you lack tech-savvy, you can hire a web designer or developer to create a custom website for your business.

They are unlikely to find your website, however, unless you follow Search Engine Optimization (SEO) practices. These are steps that help pages rank higher in the results of top search engines like Google.

Marketing

Here are some powerful marketing strategies for your future business:

Leverage Social Media Advertising: Utilize targeted social media ads to reach potential tenants based on demographics, interests, and location, ensuring your properties are visible to the right audience.

Optimize Property Listings: Craft compelling and detailed property listings with high-quality photos, emphasizing unique features and amenities, to make your rental properties stand out on online platforms.

Implement Referral Programs: Incentivize current tenants and contacts to refer prospective renters by offering discounts on rent or other perks, expanding your reach through word-of-mouth.

Host Virtual Tours: Embrace technology by providing virtual tours of your properties, allowing potential tenants to explore the space remotely, increasing engagement and saving time for both parties.

Offer Limited-Time Promotions: Create a sense of urgency by occasionally running limited-time promotions such as reduced security deposits or discounted rent for the first month, encouraging quicker tenant decisions.

Build Partnerships with Local Businesses: Forge partnerships with local businesses to cross-promote services and create mutually beneficial arrangements, increasing exposure within the community.

Collect and Showcase Tenant Testimonials: Request positive feedback from satisfied tenants and showcase their testimonials in marketing materials, boosting credibility and building trust with potential renters.

Attend Community Events: Participate in local events and sponsorships to increase your brand visibility within the community, fostering a positive reputation and attracting potential tenants.

Implement Tenant Loyalty Programs: Retain current tenants by implementing loyalty programs, offering rewards or discounts for lease renewals, creating a sense of value for long-term residents.

Utilize Email Marketing: Build an email list of potential tenants and send regular updates on available properties, promotions, and relevant local news, maintaining ongoing communication and engagement.

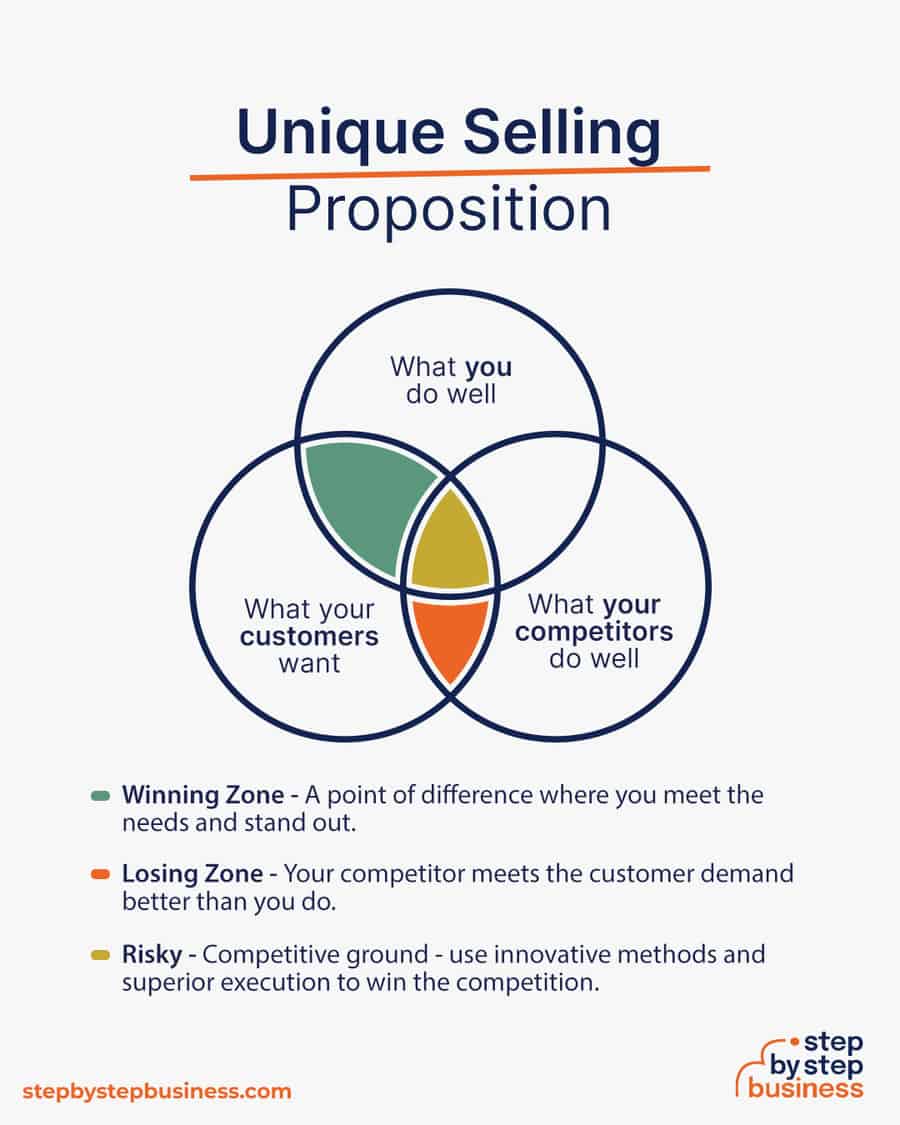

Unique selling propositions, or USPs, are the characteristics of a product or service that sets it apart from the competition. Customers today are inundated with buying options, so you’ll have a real advantage if they are able to quickly grasp how your rental property meets their needs or wishes. It’s wise to do all you can to ensure your USPs stand out on your website and in your marketing and promotional materials, stimulating buyer desire.

Global pizza chain Domino’s is renowned for its strong USP: “Fresh, hot pizza delivered in 30 minutes or less, guaranteed.” Signature USPs for your rental property business could be:

Affordable apartments in suburbia

Luxury executive home rentals

Updated urban rentals

Networking

You may not like to network or use personal connections for business gain. But your personal and professional networks likely offer considerable untapped business potential. Maybe that Facebook friend you met in college is now running a rental property business, or a LinkedIn contact of yours is connected to dozens of potential clients. Maybe your cousin or neighbor has been working in rental properties for years and can offer invaluable insight and industry connections.

The possibilities are endless, so it’s a good idea to review your personal and professional networks and reach out to those with possible links to or interest in rental properties. You’ll probably generate new customers or find companies with which you could establish a partnership. Online businesses might also consider affiliate marketing as a way to build relationships with potential partners and boost business.

12. Build a Reliable Team

If you’re starting out small from a home office, you may not need any employees. But as your business grows, you will likely need workers to fill various roles. Potential positions for a rental property business would include:

Marketing Lead – SEO strategies, social media, other property marketing

At some point, you may need to hire all of these positions or simply a few, depending on the size and needs of your business. You might also hire multiple workers for a single role or a single worker for multiple roles, again depending on need.

Free-of-charge methods to recruit employees include posting ads on popular platforms such as LinkedIn, Facebook, or Jobs.com. You might also consider a premium recruitment option, such as advertising on Indeed, Glassdoor, or ZipRecruiter. Further, if you have the resources, you could consider hiring a recruitment agency to help you find talent.

Most of us have been renters at some point in our lives, and wouldn’t it be better to be the landlord? You can provide safe housing for people and, at the same time, create a valuable real estate portfolio that can provide a steady source of income for a long time.

About a third, or 35%, of households in the United States are renters, and you can capitalize on that market with your own rental property business. In 10 years, think of what it will be worth! Now that you’re armed with insights into the business, you’re now ready to start your journey into the entrepreneurial world of being a landlord.

Can I start a rental property business with no money?

Contrary to what some companies may try to tell you at their seminars, realistically you need a down payment of 20% – 25% to buy a property. You also need to pay for any licenses or permits that may be required, and insurance, at the very least. Your investment in a rental property business, however, will be well worth it in the long run.

Do I need an LLC for a rental property business?

In short, a rental property business has risks, and without personal liability protection, your personal assets could be threatened. Choosing to form an LLC is not a requirement, but it offers many benefits for you as a business owner, such as personal liability protection. If a tenant ever sues you, that liability protection will keep your personal assets safe.

How profitable is a rental property business?

Realistically, to make a good income you need to have multiple units. A rule of thumb is to net at least $100 per month per unit. The real value you get from a rental property business comes from tax advantages and the long-term appreciation of your properties. In 10 years, you could build something that’s worth into the 7 figures!

How should I choose a property to buy as a rental?

You should look at what you can buy it for, how much your mortgage will be, and what rent you can get for it based on market rates. Generally, you should aim to net at least $100 per month per unit. You should also look at the location to see if properties in the area are appreciating since the property value is what you will really benefit from in the long run.

What rental property makes the most money?

The rental property that makes the most money can vary depending on factors such as location, market demand, property size, and rental rates. Generally, properties with high rental yields and potential for appreciation tend to generate higher profits. This can include properties in desirable locations with strong rental demand, such as apartments or homes in popular urban areas or vacation destinations.

What is the most common type of rental?

The most common type of rental property is residential rentals, such as apartments, houses, and condominiums. Residential rentals cater to individuals and families seeking long-term accommodation.

Hi, I would like to start a rental property business. I would appreciate if you let me know how to start.