Carolyn Young is a business writer who focuses on entrepreneurial concepts and the business formation. She has over 25 years of experience in business roles, and has authored several entrepreneurship textbooks.

David has been writing and learning about business, finance and globalization for a quarter-century, starting with a small New York consulting firm in the 1990s.

Published on December 30, 2021

Fast Facts

Investment range

$2,250 - $32,100

Revenue potential

$80,000 - $625,000 p.a.

Time to build

1 – 3 months

Profit potential

$70,000 - $250,000 p.a.

Industry trend

Growing

Commitment

Flexible

These crucial factors should be taken into account when you begin your title company:

Define your services — Decide on the types of services you will offer, such as title searches, title insurance, escrow services, and closing services.

Title agent license — Apply for a title agent license or permit from your state’s insurance department. Requirements vary by location and may include exams and background checks.

Surety bond — Secure a surety bond as required by your state to protect your clients from potential losses caused by fraudulent or unethical actions.

Choose a location — Select a location that is easily accessible for clients and close to real estate professionals, such as real estate agents, mortgage brokers, and attorneys.

Errors and omissions insurance — Get errors and omissions insurance to protect your business from claims related to professional errors or negligence.

Legal business aspects — Register for taxes, open a business bank account, and get an EIN.

Title software — Invest in title software to manage title searches, document preparation, and compliance.

Website and online presence — Create a professional website showcasing your services, expertise, and contact information. Offer online resources for clients, such as a blog or FAQ section, and maintain active social media profiles to engage with potential customers.

Interactive Checklist at your fingertips—begin your title company today!

Starting a title company, which handles the paperwork for funds transfers and works with title insurance underwriters to make sure everything is in legal and financial order, has pros and cons that you should consider before you decide if the business is right for you.

Pros

Flexibility – Start as a mobile title agent

Deliver Value – Provide an essential service to customers

People-Focused – Work with new people every day

Cons

Red Tape – Many documents require attention to detail

Licensing – Training and exam required

Title insurance industry trends

The pandemic forced a digital transformation of the US title insurance industry. Documents can now be notarized digitally, eliminating the need for an in-person closing. For more on digital notarization and starting your own notary, read this Step By Step article.

Funds are also being transferred electronically, eliminating the need for buyers to bring a cashier’s check to closing. Mobile title companies, meanwhile, are offering their services to mortgage brokers.

Startup costs for title companies range from $2,000 to $32,000. The lower end is the cost if you start as a mobile title agent, while the high end includes the rental and preparation of office space.

You’ll need a handful of items to successfully launch your title company. Here’s a list to get you started:

Computers

Printers and copy machines

Conference tables and chairs

Startup Costs

Ballpark Range

Average

Setting up a business name and corporation

$150 - $200

$175

Licenses and permits

$100 - $300

$200

Insurance

$100 - $300

$200

Business cards and brochures

$200 - $300

$250

Website setup

$1,000 - $3,000

$2,000

Training and licensing

$300 - $500

$400

Surety and Fidelity bonds

$400 - $1.500

$950

Office space security deposit

$0 - $6,000

$3,000

Office equipment and furniture

$0 - $20,000

$10,000

Total

$2,250 - $32,100

$17,175

How much can you earn from a title company?

Before you can start making money, you need to take the training and pass the exam to become a licensed title agent. Each state has its own requirements for licensing. Typically the process takes no more than 1-2 weeks, and will cost $75 to $200.

The typical fee paid to a title company or title insurance company at closing is about $300. As a mobile agent working from home, your profit margin should be about 90%.

In your first year or two, you could do 5 closings a week, bringing in nearly $80,000 in annual revenue. This would mean over $70,000 in profit, assuming that 90% margin. As your brand gains recognition, you’d likely rent an office and hire staff, reducing your margin to 40%. If you do 40 closings a week, your annual revenue would be almost $625,000, and you’d make a tidy profit of about $250,000.

There are a few barriers to entry for a title company. Your biggest challenges will be:

Training, studying, and passing the licensing exam

Stiff competition from large, established title companies

2. Define Your Niche

Now that you know what’s involved in starting a title company, it’s a good idea to hone your concept in preparation to enter a competitive market.

Market research will give you the upper hand, even if you’re already positive that you have a perfect product or service. Conducting market research is important, because it can help you understand your customers better, who your competitors are, and your business landscape.

Why? Identify an opportunity

Research other title companies in your area to examine their services, price points, and customer reviews. You’re looking for a market gap to fill. For instance, maybe the local market is missing a mobile title service, or a reliable title insurance business with an appealing website.

You might consider targeting a niche market by specializing in a certain aspect of your industry, such as mortgage loan refinancing or a particular type of real estate transaction or joint venture.

This could jumpstart your word-of-mouth marketing and attract clients right away.

What? Determine your services

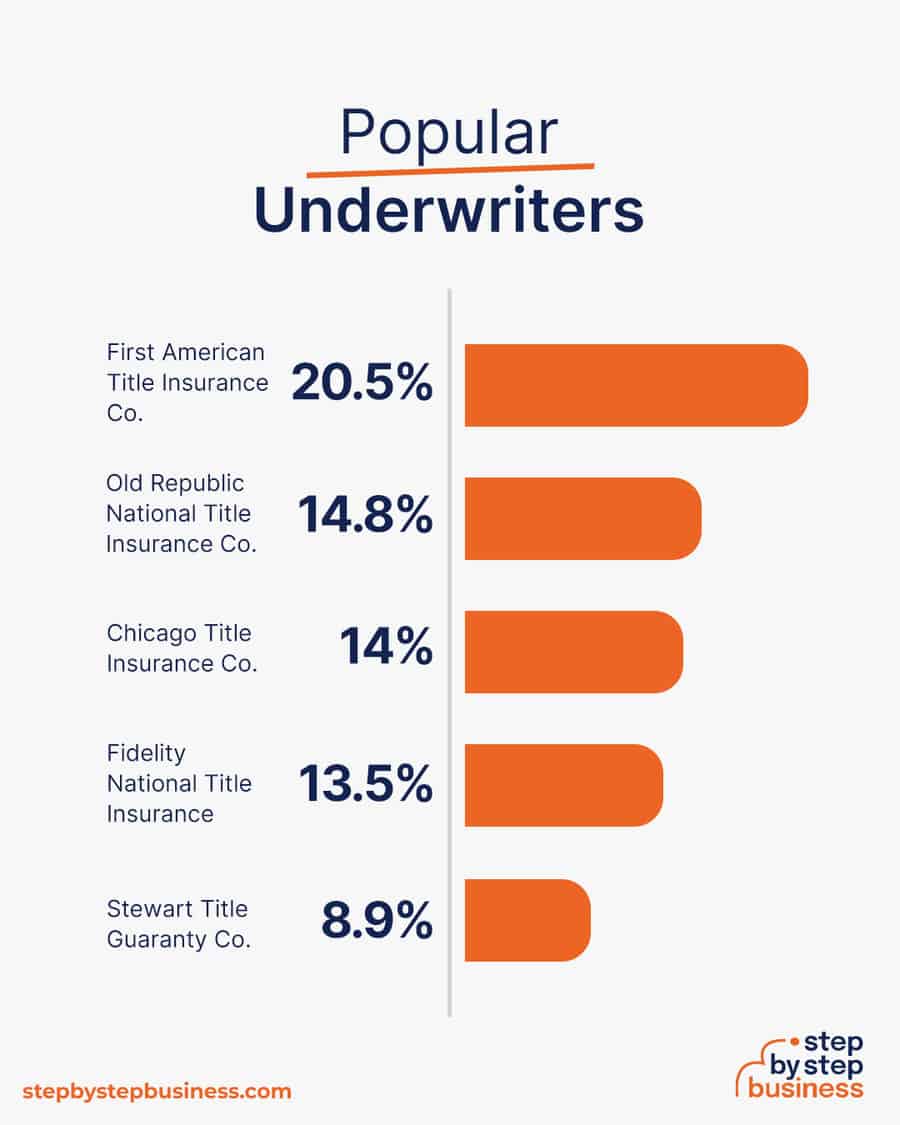

You’ll need to decide if you want to offer in-person closings, mobile closings, digital closings, or all three. You’ll also need to find a reliable title insurance underwriting company to partner with.

Four main companies, known as the Big Four, are the most used: Fidelity National Financial, First American Financial, Old Republic, and Stewart Information Services.

How much should you charge for closing services?

The average fee a title company receives for a closing is $300. As a mobile service working out of your home, your only costs will be for paperwork and fuel. When you open an office, you’ll have rent, overhead, and labor costs. You’ll still want to provide mobile services at this point, but you’ll be able to do in-person closings as well to increase your volume.

Once you know your costs, you can use this Step By Step profit margin calculator to determine your mark-up and final price points. Remember, the prices you use at launch should be subject to change if warranted by the market.

Who? Identify your target market

As a mobile service, your target market will be mainly mortgage brokers who will engage you for refinance transactions. Once you have an office for in-person closings, your target market will expand to realtors, but you’ll still want to connect with mortgage brokers for the mobile part of your business. Both of those target markets can be found on business-related sites like LinkedIn.

Where? Choose your business premises

In the early stages, you may want to run your business from home to keep costs low. But as your business grows, you’ll likely need to hire workers for various roles and may need to rent out an office. You can find commercial space to rent in your area on Craigslist, Crexi, and Commercial Cafe.

When choosing a commercial space, you may want to follow these rules of thumb:

Central location accessible via public transport

Ventilated and spacious, with good natural light

Flexible lease that can be extended as your business grows

Ready-to-use space with no major renovations or repairs needed

3. Find a Name That Builds Trust

Here are some ideas for brainstorming your business name:

Short, unique, and catchy names tend to stand out

Names that are easy to say and spell tend to do better

The name should be relevant to your product or service offerings

Ask around — family, friends, colleagues, social media — for suggestions

Including keywords, such as “title service” or “title company”, boosts SEO

Choose a name that allows for expansion: “Clear Title Solutions” over “Commercial Title Solutions”

A location-based name can help establish a strong connection with your local community and help with the SEO but might hinder future expansion

Once you’ve got a list of potential names, visit the website of the US Patent and Trademark Office to make sure they are available for registration and check the availability of related domain names using our Domain Name Search tool below. Using “.com” or “.org” sharply increases credibility, so it’s best to focus on these.

Finally, make your choice among the names that pass this screening and go ahead with domain registration and social media account creation. Your business name is one of the key differentiators that set your business apart. Once you pick your company name, and start with the branding, it is hard to change the business name. Therefore, it’s important to carefully consider your choice before you start a business entity.

Executive Summary: Highlight the main objectives and strategy of your tile installation business, focusing on providing high-quality, professional tiling services for residential and commercial properties.

Business Overview: Describe your business’s specialization in tile installation, including services for floors, walls, and other surfaces in various materials like ceramic, porcelain, and natural stone.

Product and Services: Detail the range of installation services offered, including new installations, repairs, and custom tile design work.

Market Analysis: Evaluate the demand for tile installation in your area, considering factors like construction trends, homeowner renovations, and real estate developments.

Competitive Analysis: Compare your services to other tile installers and flooring companies, highlighting your strengths in craftsmanship, material quality, or unique design offerings.

Sales and Marketing: Outline your approach to attract customers, using methods such as local advertising, partnerships with contractors, and showcasing previous work.

Management Team: Highlight the experience and qualifications of your team, especially in areas like construction, design, and project management.

Operations Plan: Describe the process of project management, from client consultations to installation and completion of the work.

Financial Plan: Provide an overview of financials, covering startup costs, pricing strategies, and revenue projections.

Appendix: Include additional documents like project portfolios, customer testimonials, or supplier agreements to support your business plan.

If you’ve never created a business plan, it can be an intimidating task. You might consider hiring a business plan specialist to create a top-notch business plan for you.

5. Register Your Company

Registering your business is an absolutely crucial step — it’s the prerequisite to paying taxes, raising capital, opening a bank account, and other guideposts on the road to getting a business up and running.

Plus, registration is exciting because it makes the entire process official. Once it’s complete, you’ll have your own business!

Choose where to register your company

Your business location is important because it can affect taxes, legal requirements, and revenue. Most people will register their business in the state where they live, but if you are planning to expand, you might consider looking elsewhere, as some states could offer real advantages when it comes to title companies.

If you’re willing to move, you could really maximize your business! Keep in mind, it’s relatively easy to transfer your business to another state.

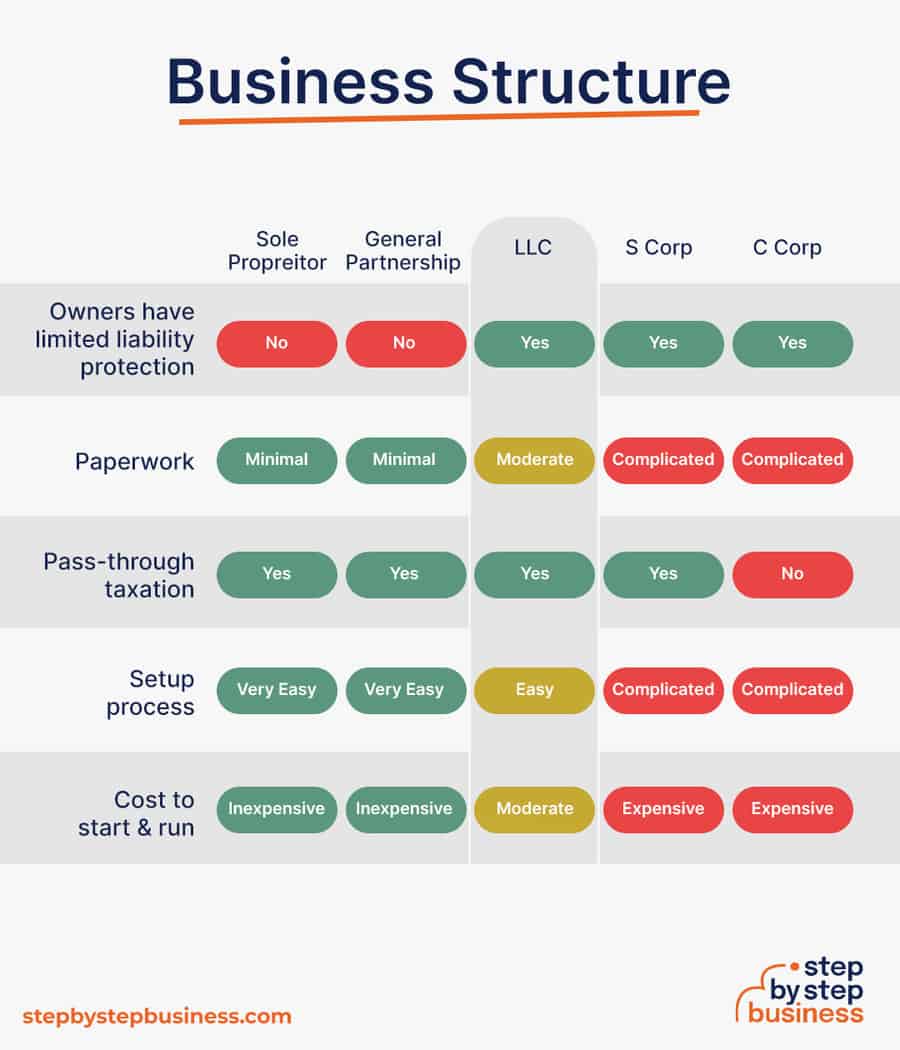

Choose your business structure

Business entities come in several varieties, each with its pros and cons. The legal structure you choose for your title company will shape your taxes, personal liability, and business registration requirements, so choose wisely.

Here are the main options:

Sole Proprietorship – The most common structure for small businesses makes no legal distinction between company and owner. All income goes to the owner, who’s also liable for any debts, losses, or liabilities incurred by the business. The owner pays taxes on business income on his or her personal tax return.

Partnership – Similar to a sole proprietorship, but for two or more people. Again, owners keep the profits and are liable for losses. The partners pay taxes on their share of business income on their personal tax returns.

Limited Liability Company (LLC) – Combines the characteristics of corporations with those of sole proprietorships or partnerships. Again, the owners are not personally liable for debts.

C Corp – Under this structure, the business is a distinct legal entity and the owner or owners are not personally liable for its debts. Owners take profits through shareholder dividends, rather than directly. The corporation pays taxes, and owners pay taxes on their dividends, which is sometimes referred to as double taxation.

S Corp – An S-Corporation refers to the tax classification of the business but is not a business entity. An S-Corp can be either a corporation or an LLC, which just needs to elect to be an S-Corp for tax status. In an S-Corp, income is passed through directly to shareholders, who pay taxes on their share of business income on their personal tax returns.

We recommend that new business owners choose LLC as it offers liability protection and pass-through taxation while being simpler to form than a corporation. You can form an LLC in as little as five minutes using an online LLC formation service. They will check that your business name is available before filing, submit your articles of organization, and answer any questions you might have.

The final step before you’re able to pay taxes is getting an Employer Identification Number, or EIN. You can file for your EIN online or by mail or fax: visit the IRS website to learn more. Keep in mind, if you’ve chosen to be a sole proprietorship, you can simply use your social security number as your EIN.

Once you have your EIN, you’ll need to choose your tax year. Financially speaking, your business will operate in a calendar year (January–December) or a fiscal year, a 12-month period that can start in any month. This will determine your tax cycle, while your business structure will determine which taxes you’ll pay.

The IRS website also offers a tax-payers checklist, and taxes can be filed online.

It is important to consult an accountant or other professional to help you with your taxes to ensure you are completing them correctly.

7. Get Funding for Startup Costs

Securing financing is your next step and there are plenty of ways to raise capital:

Bank loans: This is the most common method but getting approved requires a rock-solid business plan and strong credit history.

SBA-guaranteed loans: The Small Business Administration can act as guarantor, helping gain that elusive bank approval via an SBA-guaranteed loan.

Government grants: A handful of financial assistance programs help fund entrepreneurs. Visit Grants.gov to learn which might work for you.

Friends and Family: Reach out to friends and family to provide a business loan or investment in your concept. It’s a good idea to have legal advice when doing so because SEC regulations apply.

Crowdfunding: Websites like Kickstarter and Indiegogo offer an increasingly popular low-risk option, in which donors fund your vision. Entrepreneurial crowdfunding sites like Fundable and WeFunder enable multiple investors to fund your business.

Personal: Self-fund your business via your savings or the sale of property or other assets.

Bank and SBA loans are probably the best options, other than friends and family, for funding a title insurance business.

Starting a title company business requires obtaining a number of licenses and permits from local, state, and federal governments.

You should check your state website for education and licensing requirements to become a licensed title agent. You’ll also need to check your state’s requirements for surety and fidelity bonds. The amount of the bonds that you need will vary by state.

Federal regulations, licenses, and permits associated with starting your business include doing business as (DBA), health licenses and permits from the Occupational Safety and Health Administration (OSHA), trademarks, copyrights, patents, and other intellectual properties, as well as industry-specific licenses and permits.

You may also need state-level and local county or city-based licenses and permits. The license requirements and how to obtain them vary, so check the websites of your state, city, and county governments or contact the appropriate person to learn more.

You could also check this SBA guide for your state’s requirements, but we recommend using MyCorporation’s Business License Compliance Package. They will research the exact forms you need for your business and state and provide them to ensure you’re fully compliant.

This is not a step to be taken lightly, as failing to comply with legal requirements can result in hefty penalties.

If you feel overwhelmed by this step or don’t know how to begin, it might be a good idea to hire a professional to help you check all the legal boxes.

Before you start making money you’ll need a place to keep it, and that requires opening a bank account. Keeping your business finances separate from your personal account makes it easy to file taxes and track your company’s income, so it’s worth doing even if you’re running your title company business as a sole proprietorship.

Opening a business bank account is quite simple, and similar to opening a personal one. Most major banks offer accounts tailored for businesses — just inquire at your preferred bank to learn about their rates and features.

Banks vary in terms of offerings, so it’s a good idea to examine your options and select the best plan for you. Once you choose your bank, bring in your EIN (or Social Security Number if you decide on a sole proprietorship), articles of incorporation, and other legal documents and open your new account.

10. Set Up Business Insurance

Business insurance is an area that often gets overlooked yet it can be vital to your success as an entrepreneur. Insurance protects you from unexpected events that can have a devastating impact on your business.

Here are some types of insurance to consider:

General liability: The most comprehensive type of insurance, acting as a catch-all for many business elements that require coverage. If you get just one kind of insurance, this is it. It even protects against bodily injury and property damage.

Business Property: Provides coverage for your equipment and supplies.

Equipment Breakdown Insurance: Covers the cost of replacing or repairing equipment that has broken due to mechanical issues.

Worker’s compensation: Provides compensation to employees injured on the job.

Property: Covers your physical space, whether it is a cart, storefront, or office.

Commercial auto: Protection for your company-owned vehicle.

Professional liability: Protects against claims from a client who says they suffered a loss due to an error or omission in your work.

Business owner’s policy (BOP): This is an insurance plan that acts as an all-in-one insurance policy, a combination of any of the above insurance types.

As opening day nears, prepare for launch by reviewing and improving some key elements of your business.

Essential software and tools

Being an entrepreneur often means wearing many hats, from marketing to sales to accounting, which can be overwhelming. Fortunately, many websites and digital tools are available to help simplify many business tasks.

You can use industry-specific software, such as snapclose, eFileCabinet, or Certifid, to manage your documents, data collection, closing process, and accounting.

Popular web-based accounting programs for smaller businesses include Quickbooks, Freshbooks, and Xero.

If you’re unfamiliar with basic accounting, you may want to hire a professional, especially as you begin. The consequences for filing incorrect tax documents can be harsh, so accuracy is crucial.

Developing a website for your title company is a crucial step in expanding your market reach and brand visibility. You have two primary options: using a website builder, which is a cost-effective and user-friendly choice, particularly for those with limited technical skills, or hiring a professional web developer, which can be more expensive but offers a bespoke and potentially more sophisticated website.

Your website should highlight your services, expertise, and testimonials. Regularly update your blog with informative content about title services, real estate trends, and local market insights.

Marketing

Starting a title company requires strategic marketing to establish your presence and attract clients. Here are some effective marketing strategies tailored for your title business:

Optimize for Local SEO: Focus on local search engine optimization (SEO) to ensure your business appears at the top of search results when potential clients in your area search for title services. This includes using local keywords, optimizing your Google My Business listing, and ensuring your website is mobile-friendly.

Get Listed in Local Directories: Register your business in local online directories and platforms like Yelp, Yellow Pages, and your local Chamber of Commerce website. This increases visibility and helps build your local online presence.

Leverage Social Media: Utilize social media platforms to connect with local real estate agents, lenders, and potential clients. Share informative content, industry updates, and engage with your audience to build relationships.

Network with Real Estate Professionals: Attend local real estate events, join real estate groups, and partner with real estate agencies to get referrals. Building relationships with these professionals can lead to a steady stream of clients.

Utilize Email Marketing: Build an email list and send out regular newsletters with updates, tips, and promotions. This keeps your business top-of-mind for past and potential clients.

Host Educational Workshops: Offer free workshops or webinars on topics relevant to home buyers, sellers, and real estate professionals. This positions you as an expert in the field and helps build trust.

Engage in Community Events: Sponsor local events or participate in community activities. This increases your brand visibility and shows your commitment to the local community.

Use Targeted Online Advertising: Invest in online advertising, such as Google Ads or Facebook Ads, targeting your local area to reach potential clients actively searching for title services.

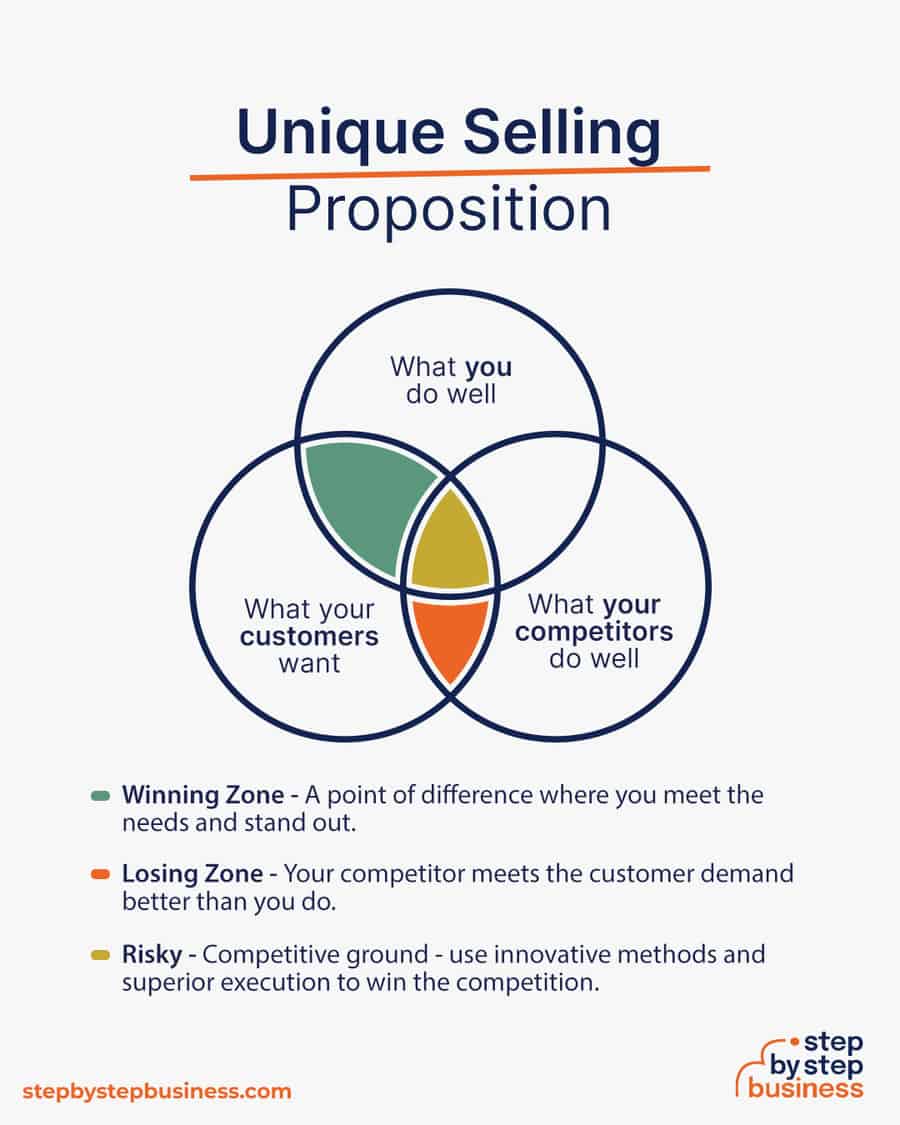

Unique selling propositions, or USPs, are the characteristics of a product or service that set it apart from the competition. Customers today are inundated with buying options, so you’ll have a real advantage if they are able to quickly grasp how your title company meets their needs or wishes. It’s wise to do all you can to ensure your USPs stand out on your website and in your marketing and promotional materials, stimulating buyer desire.

Global pizza chain Domino’s is renowned for its USP: “Hot pizza in 30 minutes or less, guaranteed.” Signature USPs for your title company could be:

Mobile title services on your time

Touchless closings, quick and easy

Closings with an expert to explain every detail

Networking

You may not like to network or use personal connections for business gain. But your personal and professional networks likely offer considerable untapped business potential. Maybe that Facebook friend you met in college is now running a title insurance business, or a LinkedIn contact of yours is connected to dozens of potential clients. Maybe your cousin or neighbor has been working in insurance or title underwriting for years and can offer invaluable insight and industry connections.

The possibilities are endless, so it’s a good idea to review your personal and professional networks and reach out to those with possible links to or interest in titles and insurance. You’ll probably generate new customers or find companies with which you could establish a partnership. Online businesses might also consider affiliate marketing as a way to build relationships with potential partners and boost business.

12. Build a Team That Knows the Industry

If you’re starting out small from a home office, you may not need any employees. But as your business grows, you will likely need workers to fill various roles. Potential positions for a title company business would include:

Title Agents – to handle closings

General Manager – scheduling, staff management

Marketing Lead – SEO strategies, social media, call realtors

At some point, you may need to hire all of these positions or simply a few, depending on the size and needs of your business. You might also hire multiple workers for a single role or a single worker for multiple roles, again depending on need.

Free-of-charge methods to recruit employees include posting ads on popular platforms such as LinkedIn, Facebook, or Jobs.com. You might also consider a premium recruitment option, such as advertising on Indeed, Glassdoor, or ZipRecruiter. Further, if you have the resources, you could consider hiring a recruitment agency to help you find talent.

13. Start Closing Deals & Growing Your Reputation!

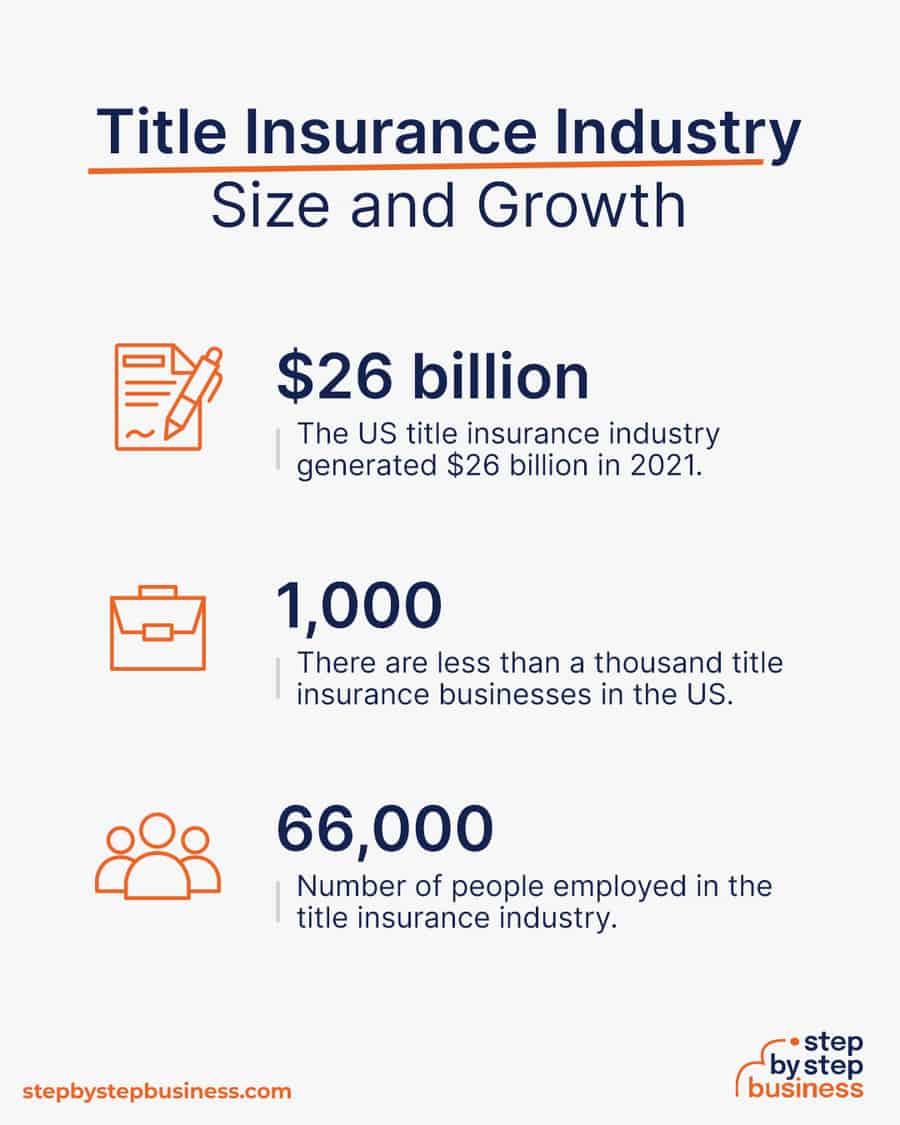

Title companies perform an essential service that protects homeowners and lenders. It’s a large industry in the US, and its market size has nearly doubled in the last decade alongside a real estate boom.

A bold entrepreneur can grab a share of this lucrative market and make good money. You can start small as a mobile service and eventually grow to have multiple brick-and-mortar locations. Startup costs are relatively low, and the process of becoming licensed does not take long.

Now that you have all the information you need, you’re ready to start your entrepreneurial journey to building a title empire!

Help Section

How do I become a licensed title agent?

Every state has its own licensing requirements. Generally, you have to complete a certain number of education hours and pass an exam. Check your state’s website for requirements.

What is title insurance?

Title insurance protects the homeowner and lender from potential defects in a title. Defects might be unsatisfied liens, legal issues, or even clerical errors.

What is the process for conducting title searches and issuing title insurance policies?

The process for conducting title searches and issuing title insurance policies involves a thorough examination of public records to determine the property’s ownership history and any potential issues. The title company resolves any problems discovered and issues title insurance policies to protect the buyer and lender from future claims or disputes.

What role does a title company play in the closing process of a real estate transaction?

A title company plays a vital role in the closing process by examining the property’s title, providing escrow services, issuing title insurance policies, and facilitating the closing meeting where documents are signed, funds are exchanged, and ownership is transferred.

How do I handle title disputes or issues that may arise during a transaction?

When a title dispute arises, a title company typically handles the situation in the following manner:

Investigation: The title company thoroughly investigates the nature of the dispute by examining the relevant title records, contracts, and other relevant documents. They may also conduct interviews with involved parties to gather additional information.

Legal Analysis: The title company consults with their in-house or external legal counsel to analyze the dispute and determine the potential legal implications. They assess the validity of the claims and review applicable laws, regulations, and contractual agreements.

Mediation and Negotiation: Depending on the circumstances, the title company may engage in mediation or negotiation with the involved parties to find a resolution. They may facilitate discussions and work towards a mutually acceptable outcome, which could involve modifying the terms of the title, reaching a settlement, or clarifying ownership rights.

Legal Defense: If the dispute escalates and legal action is initiated, the title company may provide legal defense or engage legal representation on behalf of the insured party. This can involve representing the insured party’s interests in court, presenting evidence, and arguing the case to protect the insured party’s title rights.

Financial Compensation: If the insured party experiences financial loss due to an unsuccessful defense of the title or a defect in the title, the title insurance policy may provide financial compensation to cover the damages, up to the policy’s limits and subject to its terms and conditions.

Interest in subscription.