If you’re starting an LLC, the business entity formation process is one of the first and most important hurdles. This step can be terribly complex ...

What Is an LLC?

Written by: Esther Strauss

Esther is a business strategist with over 20 years of experience as an entrepreneur, executive, educator, and management advisor.

Edited by: David Lepeska

David has been writing and learning about business, finance and globalization for a quarter-century, starting with a small New York consulting firm in the 1990s.

Published on August 6, 2021

If you are thinking about starting a business or in the process of doing so, you will soon need to decide which business entity to choose. One of the more popular entities these days is a limited liability corporation, or LLC.

This guide lays out exactly what an LLC is, its pros and cons, and how to create one, to help you decide if this is the right entity for you and your business.

What Does LLC Mean?

LLC (abbreviation) stands for Limited Liability Company, which means its members are not personally liable for the company’s debts.

LLC Defined

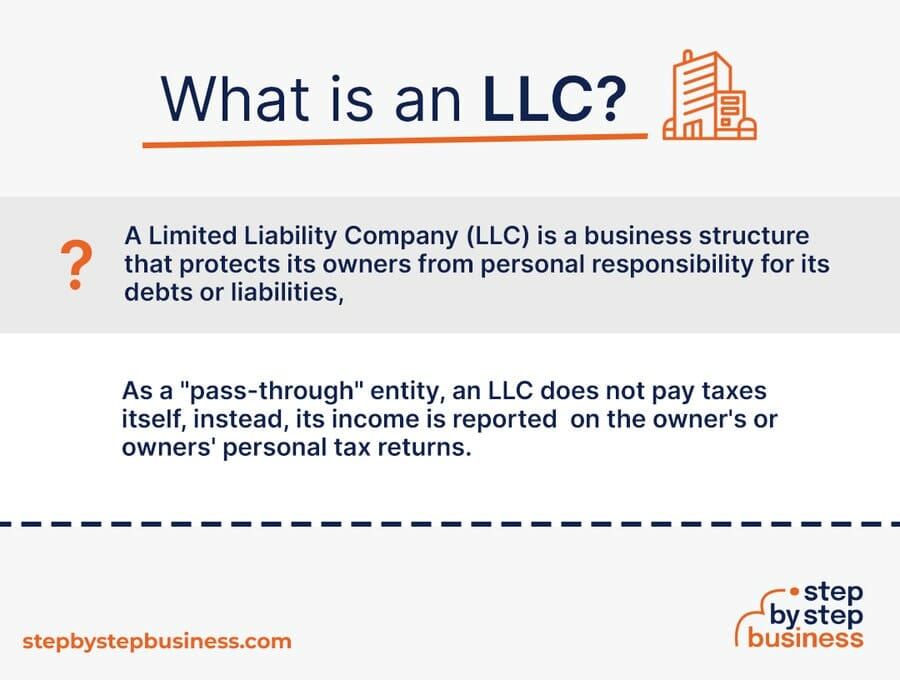

A limited liability company (LLC) is a business structure in the U.S. that protects its owners from personal responsibility for its debts or liabilities.

An LLC is an increasingly popular business structure for startups, offering liability protection for ownership and greater flexibility than a corporation, particularly in terms of taxes. The LLC itself does not pay taxes. As a “pass-through” entity, income passes through the business to the owner or owners, who report it on their personal tax returns. An LLC is created by filing paperwork with your state, and nominal fees are involved.

An LLC offers its owner or owners, who are called members, considerable flexibility in terms of management. You can choose your management and operational structure and decide how you want to be taxed.

Your LLC can have a single member or multiple members, all of whom have personal liability protection, meaning your personal assets are not at risk if you cannot pay business debts or are involved in a lawsuit.

Pros and Cons of Forming an LLC

Pros

- Simple to Form and Maintain

- Better Control of Your Business

- Limited Personal Liability

- Tax Advantages

- Profit Sharing Flexibility

- Credibility

Cons

- High Cost of Forming an LLC

- Annual Taxes and Fees Could be High

- Difficult to Transfer the Ownership of an LLC

- Not Good Legal Structure for the Investors

Read more here about the advantages and disadvantages of forming an LLC business structure.

How Are LLCs Taxed?

LLCs are unique in the context of taxation as its owners can choose how the company is taxed. Typically, an LLC is taxed like a sole proprietorship if it has one member, and a partnership if it has more than one member. However, LLCs can also be choose to be taxed as a corporation.

Electing to be taxed as a corporation is accomplished by filing a document, referred to as an election, with the Internal Revenue Services (IRS). An LLC can also be taxed as a S corporation or a C corporation.

C Corp taxes are applicable to the company profits at the tax rate for corporations. The tax rate for C Corp is 21%. This tax rate is significantly lower than the typical individual taxpayer rate.

S Corp taxation considers the LLC as a pass-through entity, in which profits pass through the company and into the hands of the owners. At this point, the taxes are applied at the same rate as those of individual taxpayers.

However, taxes for Medicare and Social Security are not applicable to these financial distributions. In the end, the S Corp tax structure is likely to result in considerable tax savings for the LLC, in comparison to C Corp.

How to Form an LLC

1. Choose Your State

The first step is to choose the state in which you plan to do business. LLC processes and requirements vary by state, so visit your state’s website for details. Generally, you can form your LLC with an online application. If you plan to have physical locations in more than one state, you will need to register a foreign LLC in the states where you will do business other than your home state.

2. Choose Your LLC Name

Your business name is extremely important. It should reflect the brand you plan to build, tell customers what you do, and be memorable. Once you’ve chosen a name, you’ll need to make sure that it’s not already taken. You can do a search on your state’s website, and on other state websites if you are doing business in more than one state. You should also check the US Patent and Trademark Office to make sure the name hasn’t been trademarked.

3. Choose a Registered Agent

A registered agent is the person or company that sends and receives legal documents on behalf of your LLC. The registered agent can be a member of the LLC, or you can choose a third party such as an attorney, or a company that offers registered agent services. Most states require you to have a registered agent. The agent must be a resident of the state where you do business, or a corporation authorized to do business in your state.

4. Determine Your Management Structure

There are two types of management structures:

- A Member-Managed LLC is managed by the members of the LLC. This is usually chosen by smaller LLCs with few members who will be involved in various management roles.

- A Manager-Managed LLC is managed by people who are not members of the LLC and are employees of the business. This structure is often used when an LLC is larger and has multiple members.

5. File Articles of Organization

The articles of organization is the form you file to create your LLC. These forms vary by state but can generally be filed online. You’ll need to fill out the LLC name, the name and address of the registered agent, the names of the LLC owners, and in some states, the way the LLC will be managed. Fees are generally around $100.

6. Draft an Operating Agreement

An operating agreement is not usually required but is highly recommended. The operating agreement should clearly define the following:

- The percentage of each member’s interests in the LLC

- How profits and losses will be allocated to each member

- Each member’s rights and responsibilities

- The management structure and management roles of members

- The voting rights of each member

- Rules for meetings and voting

- What happens when a member sells their interest, becomes disabled, or dies

It’s a good idea to have an attorney’s help when creating your operating agreement so that you can be sure you’re covering all bases to protect all members and avoid future issues.

7. Apply for Business Licenses

It’s important to make sure you’re in compliance with all laws at the local, state, and federal levels. It’s likely, depending on your location and type of business, that you’ll need business licenses and permits. Do some research to determine which licenses you need. At the very least you’ll need a sales tax permit to sell products and collect sales tax.

8. Obtain an EIN

EIN stands for Employer Identification Number and is like a social security number for your business, allowing the IRS to identify your business easily. It is also known as a Federal Tax Identification Number (FTIN), or sometimes for corporations a Tax Identification Number (TIN). An EIN is required if your LLC has more than one member, if you plan to hire employees, or if you choose to have your LLC taxed as a corporation. The application is free and can be found on the IRS website. The application is form SS-4, and it can be mailed to the IRS or submitted electronically, and once your information on the application has been validated, the EIN is assigned immediately.

After Forming an LLC

Your state may require you to file annual reports for your LLC, which may involve a fee. Check your state for requirements.

You should now be ready to form your own an LLC! And if you decide against it, that’s fine too – other entities offer advantages as well.

FAQs

What is the owner of an LLC called?

Any individual who has a share of ownership in a limited liability company (LLC) is known as a “member”. The owner or owners may have other titles as well. You should define the management structure of your LLC in your operating agreement. When the management structure is defined in the operating agreement, you can choose titles for your LLC managers.

How many owners can an LLC have?

An LLC can have an unlimited number of members unless it is taxed as an S Corp. With S-Corp status, the LLC can only have 100 or fewer members. The operating agreement will clearly define the ownership percentages of the members and the rights of the members.

Subscribe to Our Newsletter

Join our exclusive community! Subscribe to our newsletter

and gain insider access to cutting-edge business insights and trends.

and gain insider access to cutting-edge business insights and trends.

Thank you for subscribing! We can't wait to share our latest news and updates with you. Get ready for exciting content in your inbox.

Featured Resources

10 Best LLC Formation Services

Published on August 22, 2022

Read Now

17 Common Tax Deductions (Write-Offs) for an LLC

Published on February 15, 2022

If you’ve recently started a business and formed a limited liability company (LLC), at some point you’ll have to start thinking about taxes.Rega ...

Read Now

5 Best States to Form an LLC

Published on December 22, 2021

If you’re starting a new company and have decided to form a limited liability company (LLC), you may have heard that some states have advantageswh ...

Read Now

Comments